All Categories

Featured

Table of Contents

Similar to any kind of various other long-term life policy, you'll pay a regular costs for a final expenditure plan in exchange for an agreed-upon fatality benefit at the end of your life. Each service provider has different regulations and choices, however it's fairly simple to handle as your recipients will certainly have a clear understanding of exactly how to spend the cash.

You may not require this kind of life insurance. If you have permanent life insurance policy in area your last expenses might already be covered. And, if you have a term life policy, you may have the ability to convert it to a permanent policy without a few of the additional actions of getting last expenditure coverage.

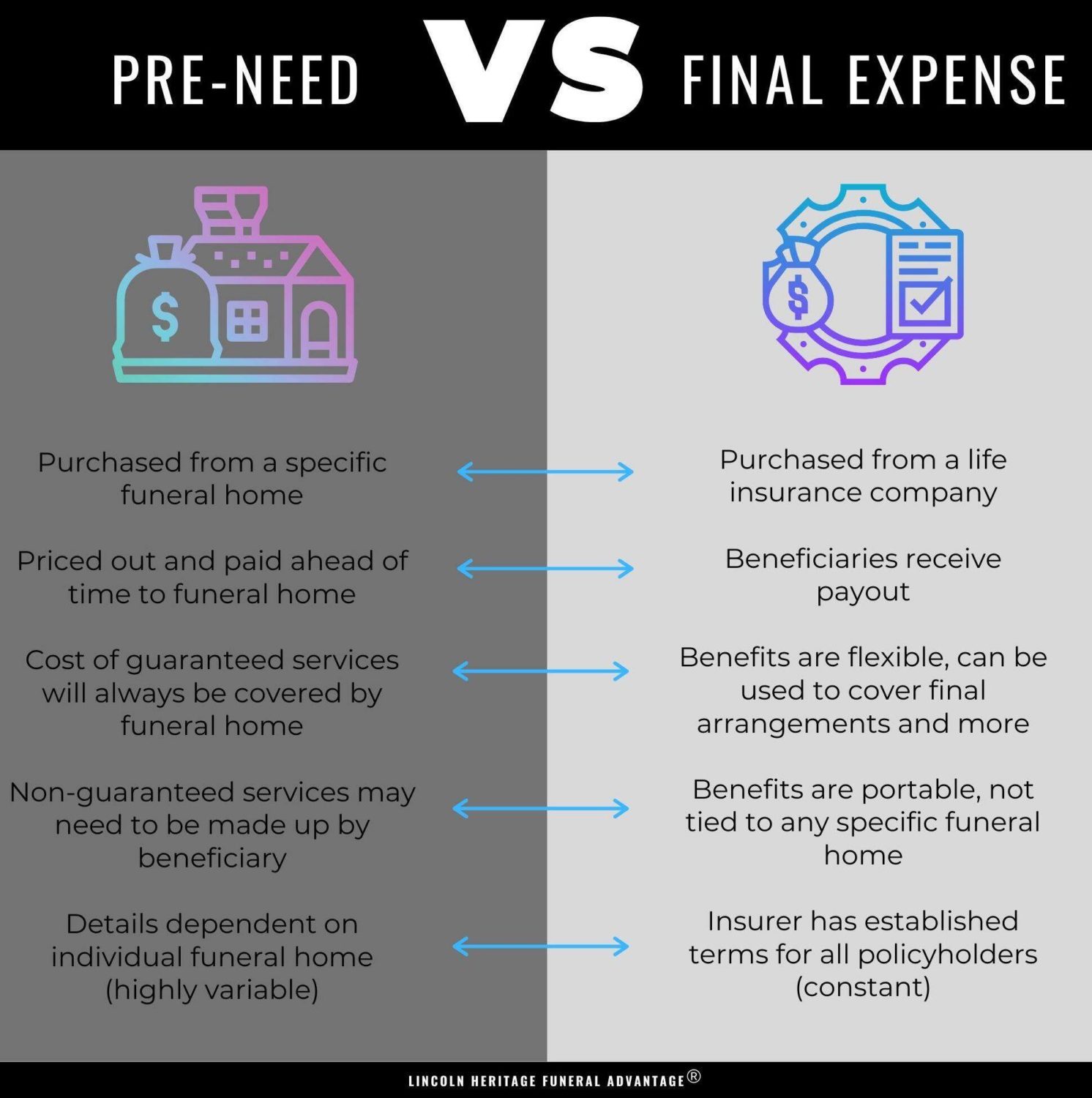

Developed to cover minimal insurance policy needs, this kind of insurance coverage can be a budget friendly alternative for individuals that just want to cover funeral expenses. (UL) insurance policy continues to be in place for your entire life, so long as you pay your premiums.

Does Life Insurance Pay For Funeral Expenses

This option to final cost protection supplies options for added household protection when you need it and a smaller sized coverage amount when you're older.

Last costs are the costs your family pays for your interment or cremation, and for various other points you might desire during that time, like a celebration to commemorate your life. Although considering last expenses can be hard, understanding what they set you back and ensuring you have a life insurance policy plan big enough to cover them can aid spare your family a cost they might not be able to afford.

United Home Life Final Expense

One choice is Funeral service Preplanning Insurance which enables you pick funeral services and products, and fund them with the purchase of an insurance plan. Another alternative is Last Cost Insurance. This kind of insurance coverage gives funds straight to your recipient to assist pay for funeral service and other costs. The quantity of your last costs depends upon numerous things, including where you stay in the United States and what sort of final setups you want.

It is forecasted that in 2023, 34.5 percent of family members will choose funeral and a higher portion of households, 60.5 percent, will certainly choose cremation1. It's approximated that by 2045 81.4 percent of family members will pick cremation2. One reason cremation is becoming extra prominent is that can be much less expensive than interment.

Final Expense Insurance Quote

Depending upon what your or your family members want, points like burial stories, grave markers or headstones, and coffins can boost the price. There may also be costs in addition to the ones specifically for funeral or cremation. They could consist of: Covering the price of travel for family members and liked ones so they can go to a service Catered dishes and other expenditures for a party of your life after the service Acquisition of unique clothing for the solution Once you have a great idea what your last costs will be, you can help get ready for them with the appropriate insurance coverage plan.

Medicare just covers clinically required costs that are required for the diagnosis and treatment of an ailment or condition. Funeral expenses are not taken into consideration clinically needed and therefore aren't covered by Medicare. Last cost insurance coverage uses a simple and fairly low-cost way to cover these costs, with plan advantages ranging from $5,000 to $20,000 or even more.

Individuals generally buy final expense insurance with the purpose that the beneficiary will utilize it to pay for funeral prices, arrearages, probate costs, or various other related costs. Funeral expenses could consist of the following: People usually question if this kind of insurance protection is necessary if they have savings or other life insurance.

Life insurance policy can take weeks or months to payment, while funeral service costs can start accumulating right away. The recipient has the last say over just how the cash is made use of, these plans do make clear the insurance policy holder's intention that the funds be utilized for the funeral and relevant prices. People usually buy permanent and term life insurance policy to assist provide funds for recurring expenditures after an individual dies.

Secure Final Expense Scams

The very best method to ensure the policy amount paid is invested where meant is to call a beneficiary (and, in some cases, a second and tertiary beneficiary) or to place your dreams in a making it through will certainly and testament. It is usually an excellent method to inform main beneficiaries of their anticipated obligations once a Last Expense Insurance coverage policy is obtained.

Costs start at $22 per month * for a $5,000 coverage policy (premiums will certainly vary based on problem age, gender, and insurance coverage amount). No medical examination and no health inquiries are required, and customers are assured protection through automatic certification.

To find out more on Living Benefits, click on this link. Insurance coverage under Guaranteed Concern Whole Life insurance coverage can normally be finalized within two days of preliminary application. Start an application and purchase a plan on our Guaranteed Issue Whole Life insurance policy DIY page, or call 800-586-3022 to speak to a qualified life insurance policy agent today. Listed below you will find some often asked questions should you select to make an application for Last Cost Life Insurance Policy on your very own. Corebridge Direct certified life insurance policy representatives are waiting to address any type of added inquiries you may have pertaining to the security of your liked ones in the event of your passing.

The kid cyclist is bought with the concept that your youngster's funeral costs will certainly be fully covered. Kid insurance coverage motorcyclists have a death benefit that varies from $5,000 to $25,000. When you're regreting this loss, the last thing you require is your financial debt adding difficulties. To buy this cyclist, your youngster has their own standards to satisfy.

Globe Life Final Expense

Note that this plan only covers your kids not your grandchildren. Final expense insurance coverage plan benefits do not finish when you sign up with a plan.

Motorcyclists consist of: Faster fatality benefitChild riderLong-term careTerm conversionWaiver of costs The increased death benefit is for those that are terminally ill. If you are seriously sick and, depending on your details policy, determined to live no longer than six months to two years.

The Accelerated Fatality Benefit (in the majority of situations) is not strained as income. The disadvantage is that it's mosting likely to decrease the survivor benefit for your recipients. Getting this additionally calls for evidence that you will certainly not live previous six months to two years. The child motorcyclist is bought with the idea that your kid's funeral expenses will be fully covered.

Coverage can last up till the child turns 25. The lasting treatment biker is similar in principle to the sped up fatality benefit.

Final Expense Whole Life Insurance

This is a living benefit. It can be obtained versus, which is extremely useful because long-lasting treatment is a considerable expenditure to cover.

The incentive behind this is that you can make the switch without undergoing a medical examination. And since you will no longer get on the term policy, this additionally means that you no more need to bother with outliving your policy and losing on your survivor benefit.

Those with existing wellness conditions may encounter higher costs or constraints on protection. Keep in mind, policies normally top out around $40,000.

Consider the month-to-month premium payments, yet also the satisfaction and financial safety it supplies your household. For numerous, the reassurance that their liked ones will not be strained with monetary challenge throughout a difficult time makes last cost insurance policy a beneficial financial investment. There are two sorts of final expense insurance policy:: This kind is best for individuals in fairly healthiness that are looking for a way to cover end-of-life expenses.

Coverage amounts for streamlined issue policies typically increase to $40,000.: This kind is best for individuals whose age or health and wellness avoids them from buying various other kinds of life insurance policy coverage. There are no health needs in any way with ensured problem policies, so any person that satisfies the age requirements can normally certify.

Below are a few of the aspects you must think about: Assess the application process for various plans. Some may need you to answer health concerns, while others provide guaranteed problem alternatives. See to it the carrier that you choose provides the amount of protection that you're looking for. Look right into the repayment options offered from each provider such as monthly, quarterly, or yearly premiums.

{kind=link}

Latest Posts

What Does A 20 Year Term Life Insurance Mean

10 Year Level Term Life Insurance

What Is Optional Term Life Insurance